- Bottom Line Investing

- Posts

- Deep Dive into the Top 5 Stocks Fueling Global Energy Trade

Deep Dive into the Top 5 Stocks Fueling Global Energy Trade

Riding the Wave of Global Energy Demand

Sean O'Reilly

August 15, 2024

In partnership with

Image Made with Grok

Dear Fellow Investor,

Today we’re continuing this week’s series on how to profit off the massive disconnect between domestic and foreign natural gas prices.

We’ve already covered why this situation exists and identified our publicly-traded investment options.

Now, we’re going to look at these options from a technical and fundamental perspective.

Let’s do this.

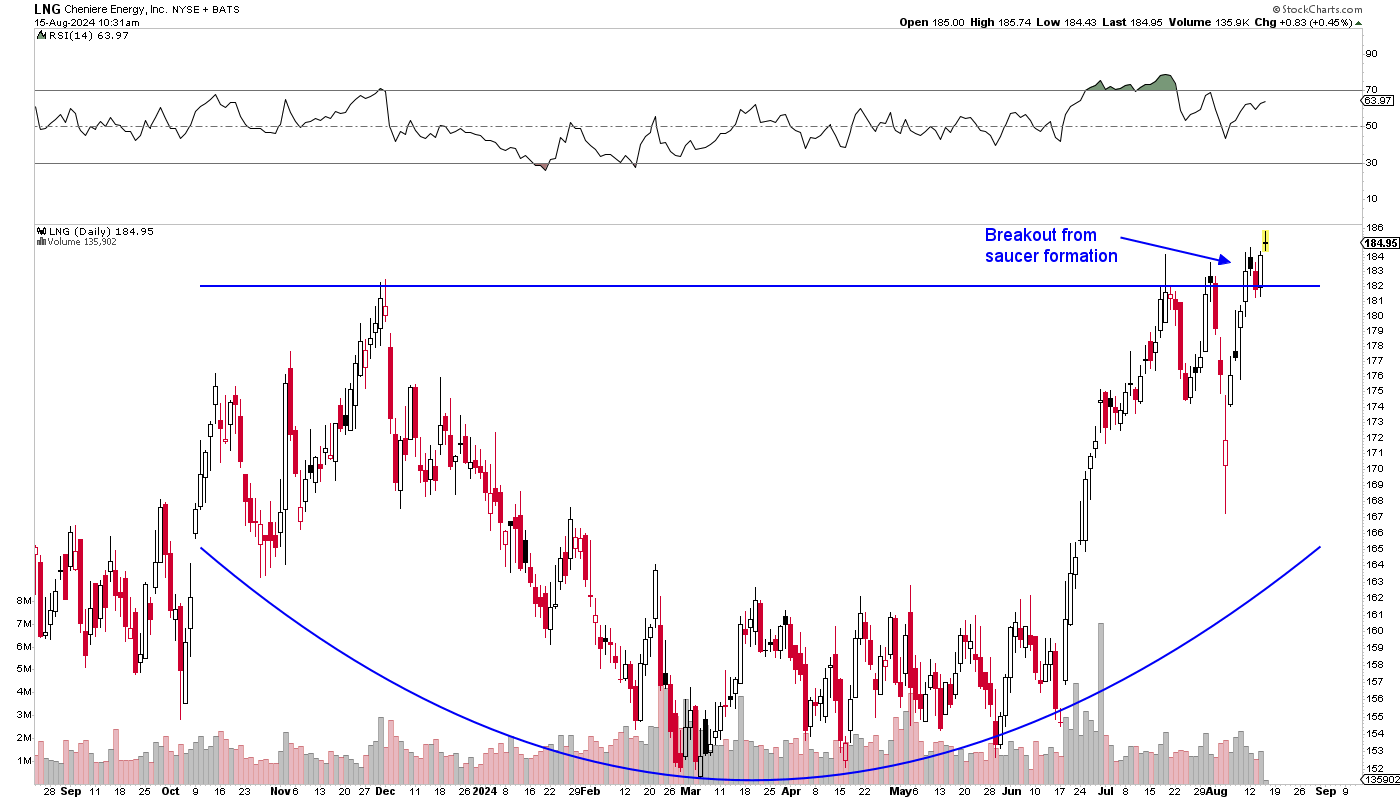

#1. Cheniere Energy (LNG)

Cheniere Energy recently broke out from what technical traders call a “saucer” formation. This is a very bullish development technically and implies that an acceleration of upside momentum is underway. The pattern is projecting a rally as high as 225.00-230.00.

Taking a look at LNG’s operations, things are expected to remain stable for Cheniere Energy until growth picks up in late 2024. The company will continue supplying natural gas to its existing international customers, but has limited extra supply for the spot market, where prices are usually higher. However, Cheniere could ramp up additional production later this year, including bringing Train 1 of the Sabine Pass mid-size trains online, provided construction stays on track. In the meantime, costs are anticipated to remain consistent, although a focus on debt reduction should boost profitability by lowering interest expenses in the coming quarters. The company also benefited from elevated fuel prices throughout 2023, and earnings are projected to reach $10.00+ per share this year.

Looking towards the end of the decade, Cheniere’s growth will be fueled by its ongoing capital projects. The company aims to complete seven mid-size trains at Sabine Pass by 2026 and has proposed further expansions at other facilities. Reducing debt remains a priority, which should continue to cut interest expenses.

Additionally, a strong share buyback program, including the recent repurchase of 7.5 million shares for approximately $1.2 billion, is expected to drive growth in earnings per share. Forecasts suggest earnings could rise to $13.50 per share in 2025 and reach $17.00 per share between 2027 and 2029.

LNG is a strong contender.

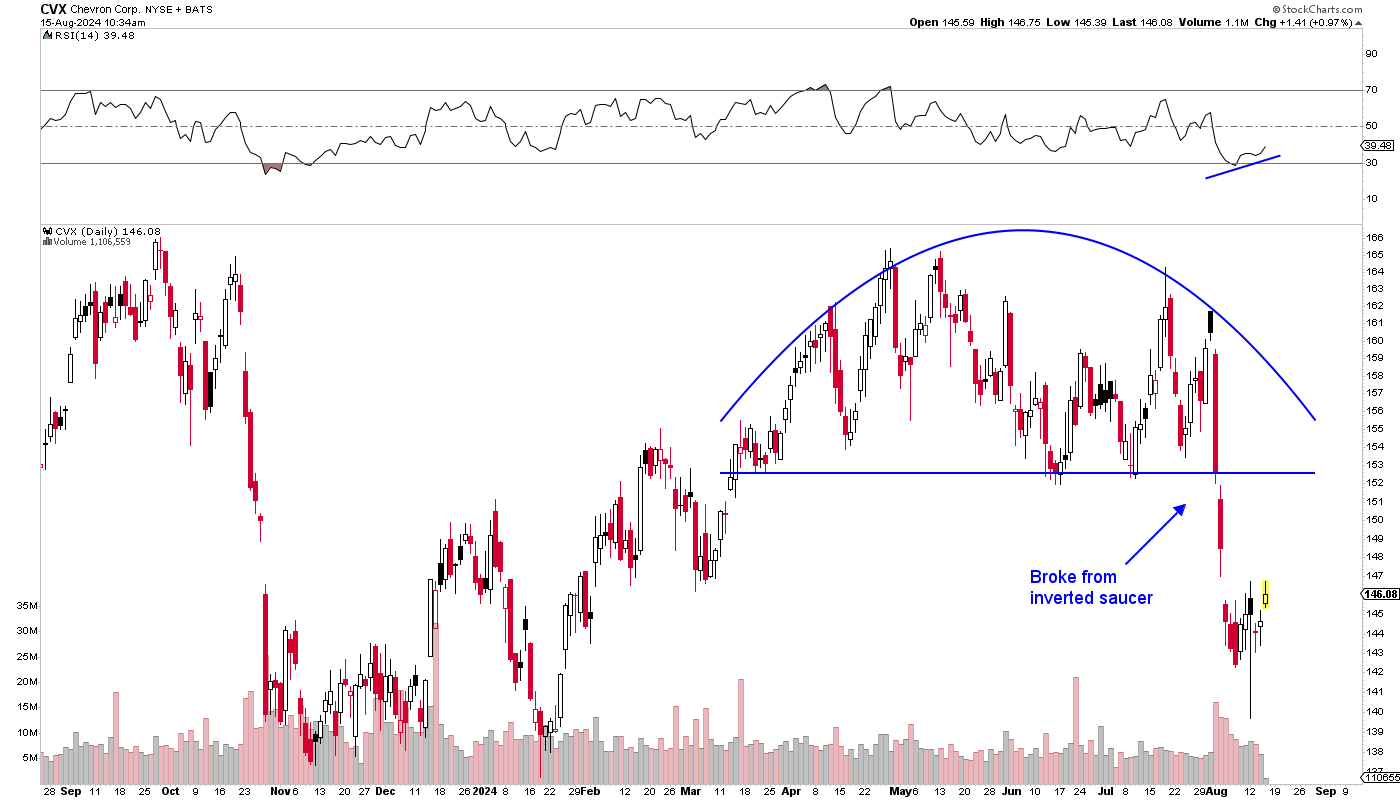

#2: Chevron (CVX)

Chevron broke down from an inverted saucer pattern, but satisfied the downside projection in the 140.00-142.00 zone. But now we have a case of bullish divergence in price from the RSI indicator at the August 12 low, signaling that downside momentum has waned. If CVX rises back above 152.00-154.00, it will turn bullish again.

Chevron's merger with Hess has been delayed by approximately six months. The two companies have pushed back their anticipated completion date from April 18th to October 22nd due to additional information requests from the Federal Trade Commission.

Despite these challenges, Chevron remains confident in closing the deal, asserting that Exxon's claims are not relevant in this context. Hess shareholders, as of April 12th, are set to vote on the merger on May 28th. The original $53 billion deal was reached last October. If the transaction is completed, it would strengthen Chevron's asset portfolio and begin contributing to cash flow per share starting in 2025. The combined entity is also expected to ramp up initiatives aimed at enhancing shareholder returns.

In other developments, Chevron reported lower sales and earnings per share in the first quarter. The decline was driven by narrower margins in refined product sales and lower natural gas prices. However, increased upstream sales volumes in the United States and a 12% rise in global production provided some offset. Nonetheless, projections for full-year 2024 have been adjusted downward, with expected sales and earnings per share now forecasted to decline by 3% and 6%, respectively.

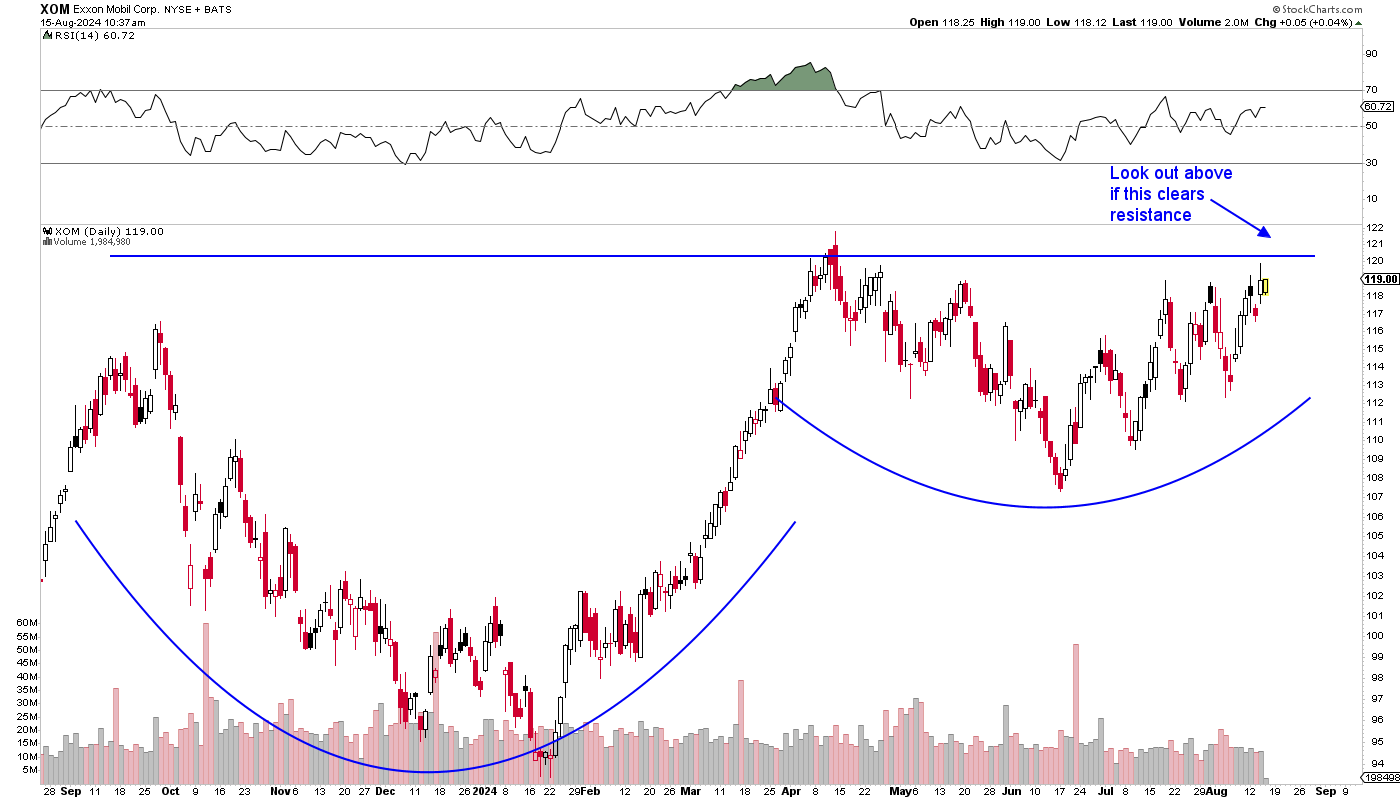

#3: Exxon Mobil (XOM)

Exxon Mobil is postured in a very bullish manner here with prices on the precipice of breaking out from a cup and handle formation. A close above 120.00-121.00 would be very bullish and could lead to another leg higher into the 150.00-155.00.

Exxon Mobil posted stronger-than-expected earnings in the first quarter of 2024, reporting $2.06 per share, surpassing the earlier forecast of $1.80. Despite narrower refining margins due to lower commodity prices, effective cost controls and operational enhancements supported profitability. Additionally, robust upstream production, particularly in Guyana, along with the expansion at the Beaumont refinery, contributed positively. As a result, the full-year earnings estimate has been raised by $0.25, bringing it to $9.50 per share. Exxon Mobil's stock has been trading near record highs, having rebounded over 10% since late February and continuing to fluctuate between $95 and $120.

The company recently completed its acquisition of Pioneer Natural Resources, with Pioneer shareholders receiving 2.3234 shares of Exxon Mobil for each share owned. This acquisition significantly increases Exxon’s footprint in the Permian Basin. It’s interest that, in accordance with FTC conditions, Pioneer’s CEO is barred from joining Exxon’s board due to past allegations of collusion with OPEC officials.

Looking forward, Exxon Mobil remains well-positioned for sustained success. Traditional oil and gas operations are expected to perform well, supported by favorable macroeconomic trends and steady consumer demand, despite the outlook for softer commodity prices.

Moreover, the company’s accelerated focus on alternative energy is set to pay off, with recent investments directed toward lithium battery technologies, carbon capture, and expanding solar and wind projects. Overall, these strategic moves should result in a well-diversified energy portfolio by the late 2020s.

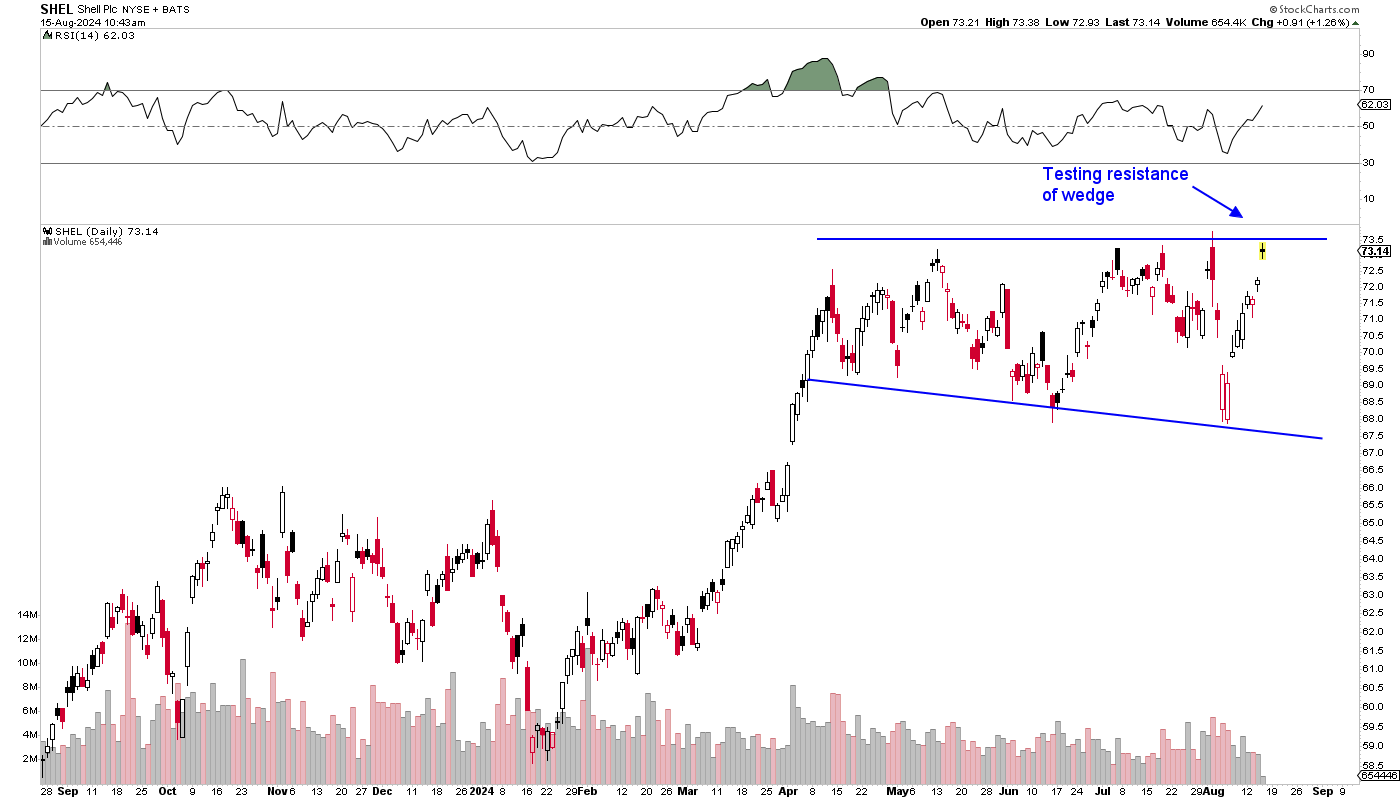

#4: Shell (SHELL)

Shell is testing resistance of a broadening wedge formation. These are momentum patterns, and if it can manage a close above 74.00-75.00, then a measured move into the 90.00-92.00 zone should follow at the least.

Shell experienced a strong recovery in its earnings during the first quarter of 2024. After a challenging end to 2023, the energy giant began the year on a positive note, with earnings of $2.28 per ADR, significantly exceeding expectations and showing a substantial improvement from the previous period. Refining margins remained solid despite volatile commodity prices, and a reduction in operating costs further boosted profitability. As a result, the full-year earnings forecast has been revised upward to $7.45 per ADR, compared to the earlier estimate of $6.65.

Investor sentiment towards Shell is increasingly positive. Over the past three months, the ADRs have gained over 15% in value, reaching new 52-week highs and levels not seen since before the pandemic. Additionally, Shell’s shareholder-friendly policies remain intact. The company has been actively reducing its ADR count and is likely to continue its stock buyback program. Moreover, even at its current elevated price, Shell’s dividend yield remains well above average.

In a strategic move, Shell is divesting its refinery and petrochemical assets in Singapore. The sale includes a refinery and an ethylene plant, which will be acquired by an Indonesia-based joint venture and Glencore for an undisclosed sum. The transaction is expected to close by the end of 2024.

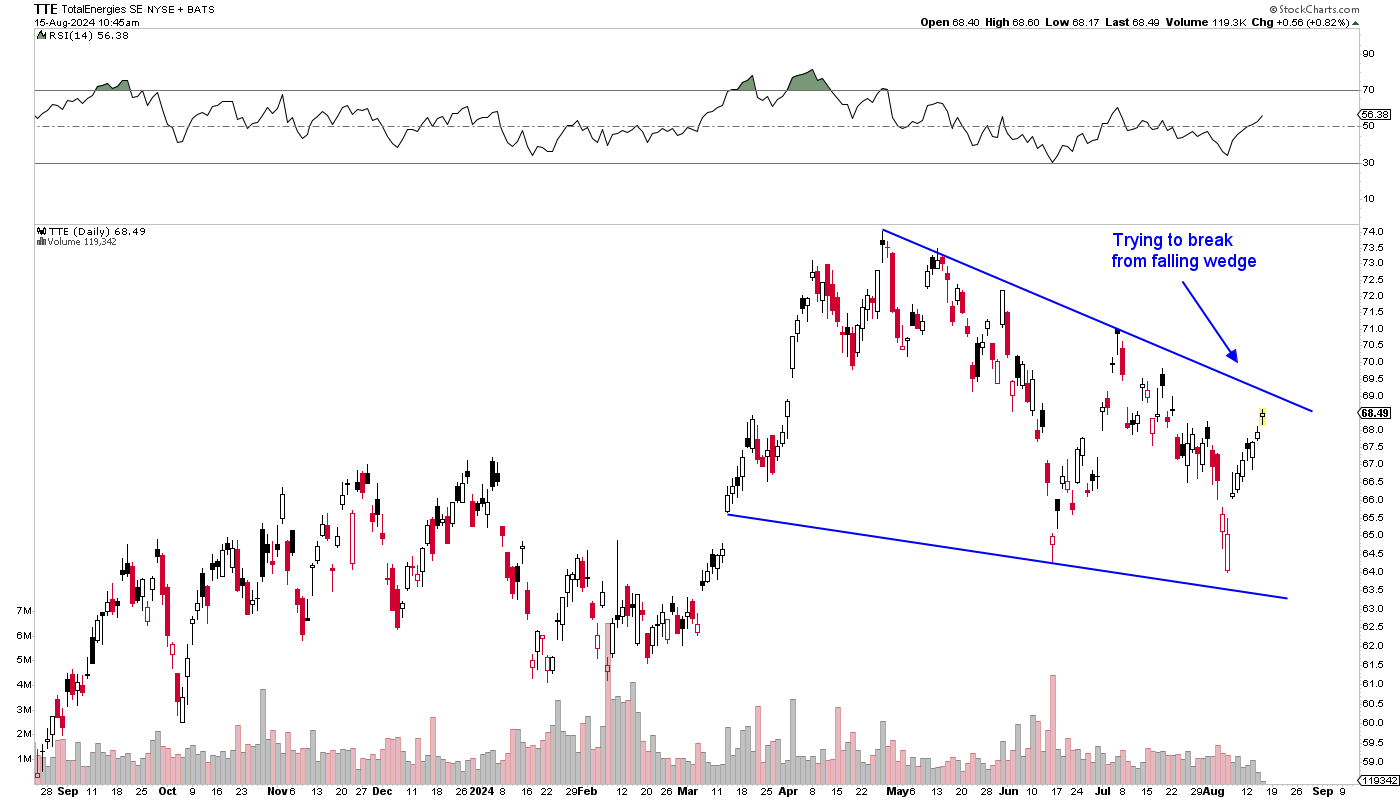

#5: TotalEnergies SE (TTE)

TotalEnergies has gone through a corrective rally over the past 3 months or so, and in the process, formed a falling wedge formation. If prices break above the upper trendline of the pattern, then a rally up to the 84.00-85.00 area could follow.

TotalEnergies has seen a strong rise in its stock price over the last three months, with its ADRs gaining around 15% as investors have responded positively to the company’s recent financial results. The stock has recently reached new 52-week highs and is trading at levels not seen in nearly a decade.

First-quarter results were solid, particularly considering the challenges of fluctuating commodity prices. TotalEnergies posted sales of $56.3 billion for the quarter, slightly below expectations. However, earnings of $2.40 per ADR represented a 9% year-over-year increase and comfortably exceeded consensus forecasts. This growth was driven by strong refining margins, stable production, and lower inventory costs. Analysts expect EPS to come in between $7-$8 per share this year.

The company plans to continue its stock buybacks, supported by its recent profitability. Management has announced a new buyback authorization and has also committed to annual increases in the quarterly dividend. While investments in alternative energy are expected to rise over the long term, traditional oil and gas operations will remain the primary growth engines.

All in all, TotalEnergies is poised to make further advances in low-carbon technologies, battery storage, and power generation solutions. In the near term, both downstream and upstream operations (including the export of LNG) are likely to accelerate as global energy demand grows under more favorable macroeconomic conditions.

Until Tomorrow,

Sean O’Reilly

Disclosure: This content is for educational purposes only and should not be construed as financial advice. Sean O'Reilly may have positions in some of the stocks discussed in this post. Please conduct your own research or consult a financial advisor before making any investment decisions.

We put your money to work

Betterment’s financial experts and automated investing technology are working behind the scenes to make your money hustle while you do whatever you want.